TL;DR:

- "Guaranteed approval" for cabin financing is a marketing myth because all legitimate lenders require income and financial review.

- Manual underwriting and pre-approval programs that assess income and assets before credit checks open new possibilities for buyers with poor or no credit.

If you've been searching for "understanding guaranteed approval cabins," you've probably hit a wall of confusing promises and fine print. The phrase gets used loosely across very different contexts, from cruise ship bookings to short-term rental permits to manufactured home financing, and that muddiness causes real problems for buyers who need honest answers. This article cuts through the noise. You'll learn exactly what guaranteed approval means in the cabin financing world, what lenders actually evaluate, and what steps put you in the strongest position to get approved without chasing misleading claims.

Table of Contents

- Key takeaways

- Understanding guaranteed approval cabins: what the term really means

- Why "guaranteed approval" loans don't actually exist

- How manual underwriting opens doors for buyers without strong credit

- Financing programs that skip the upfront credit inquiry

- What to do before you apply for cabin financing

- My honest take on guaranteed approval cabin claims

- Get started with Ez-cabin's flexible financing today

- FAQ

Key takeaways

| Point | Details |

|---|---|

| "Guaranteed approval" isn't literal | No legitimate lender can approve a cabin loan without reviewing your income or financial history. |

| Credit checks are deferred, not gone | "No credit check" programs typically defer the pull, not eliminate it. Ask when it happens. |

| Manual underwriting opens real doors | Lenders can approve buyers with weak credit using rent history, utility payments, and stable income. |

| Preparation beats promises | Gathering documents before applying puts you ahead of buyers chasing guaranteed approval myths. |

| Ez-cabin's rent-to-own changes the math | Only the first month's payment is needed to start, with no traditional credit check required. |

Understanding guaranteed approval cabins: what the term really means

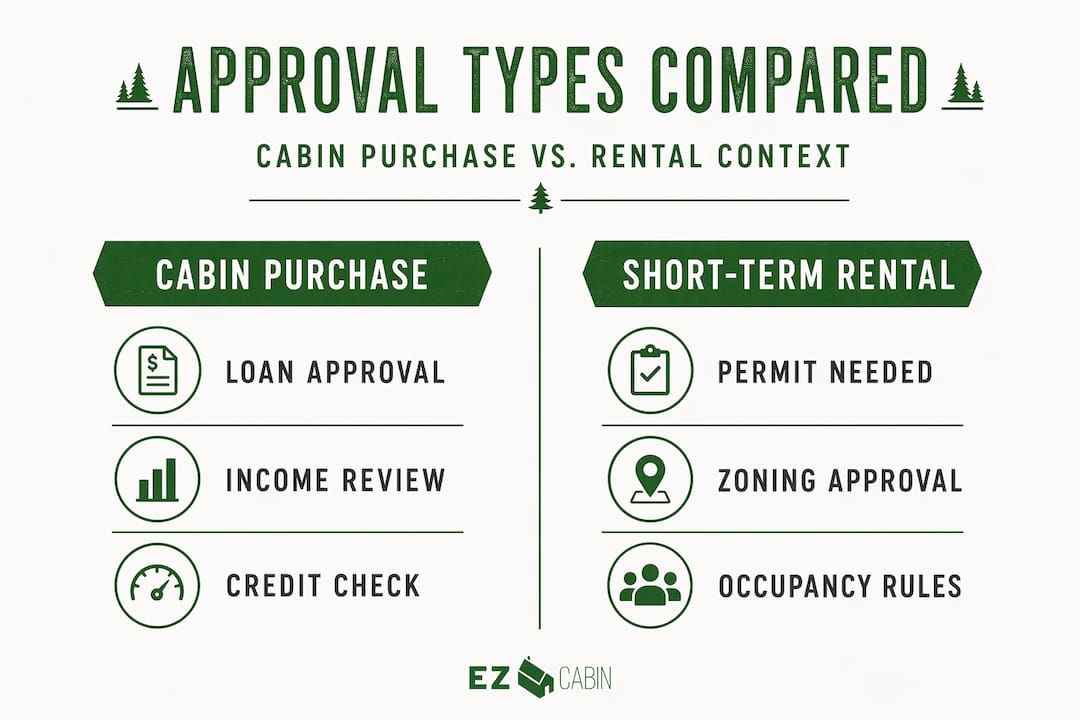

The phrase "guaranteed approval cabins" pulls in three completely different meanings depending on where you're searching, and confusing them wastes serious time.

The first meaning comes from cruise travel. Guaranteed cabin bookings refer to cruise lines assigning you a cabin category rather than a specific room. You're guaranteed a cabin type, not a particular spot on the ship. This has nothing to do with financing.

The second meaning involves short-term rental approvals. In many counties and municipalities, you need a permit or planning approval before renting a cabin on platforms like Airbnb or VRBO. That process involves local zoning rules, fire safety checks, and sometimes neighborhood review boards. Understanding cabin rental approval in this context is about regulatory compliance, not credit scores.

The third meaning is the one most people searching for this topic actually need: cabin financing approval. This is where a lender evaluates whether you qualify to purchase a manufactured cabin, portable building, or tiny home through a loan or rent-to-own program. It's also where the most confusion and deception lives.

Here's what distinguishes these three contexts at a glance:

- Cruise cabins: Guaranteed category assignment, no financial approval involved

- Short-term rental permits: Local government approval, based on zoning and safety compliance

- Cabin financing: Lender approval based on income, credit, and repayment ability

- Rent-to-own programs: Retailer-based agreements with different criteria than bank loans

Getting clear on which kind of approval you're actually seeking shapes every decision you make from here forward. For most people reading this, cabin financing approval is the real goal.

Why "guaranteed approval" loans don't actually exist

This is where honesty matters more than marketing. No legitimate lender can offer guaranteed approval for manufactured home financing. Every loan product on the market, even the most flexible ones, requires some level of underwriting. That means someone evaluates your ability to repay before money changes hands.

The underwriting process looks at several factors. Income is the biggest one: lenders need to see that you earn enough to cover the monthly payment. They also review your existing debts, the value and condition of the property, and yes, your credit. Even products marketed as "easy approval cabins" or "no credit check" financing go through some version of this review.

"Guaranteed approval is not available. Be cautious of any lender claiming guaranteed approval or instant approval without any credit check, as these offers are often deceptive." — Acorn Finance

The phrase "no credit check" is where things get especially misleading. Credit pulls are deferred, not eliminated in most of these programs. A lender reviews your income and scenario first, and if it looks workable, then they pull credit before issuing final approval. That's a meaningful difference from never checking credit at all.

What should you watch for? Red flags include lenders demanding large upfront fees before approval, promises of 100% approval regardless of income, and vague terms that never specify when or how a credit review happens. These are signs of predatory lending, not genuine flexibility.

Pro Tip: Before applying anywhere, ask the lender directly: "At what stage does a credit pull happen?" A straight answer protects your credit score and tells you whether you're dealing with a transparent program.

Understanding cabin financing approval means accepting that no magic shortcut exists. But that doesn't mean buyers with poor credit or no credit history are out of options. Far from it.

How manual underwriting opens doors for buyers without strong credit

Manual underwriting is the most powerful tool available to buyers who can't pass an automated credit scoring system. Instead of running your application through software that spits out a yes or no based on your FICO score, a human underwriter reviews your complete financial picture.

Here's how the process works in practice:

- You submit documentation of your income (pay stubs, tax returns, or bank statements for self-employed buyers).

- The underwriter reviews your rent payment history, ideally verified by a landlord letter or 12 months of canceled checks.

- Utility payments, insurance premiums, and phone bills are used as non-traditional credit tradelines to demonstrate responsible financial behavior.

- The underwriter looks at compensating factors: your cash reserves, the size of your down payment, and whether your monthly payment represents a manageable increase from your current rent.

- A final decision is made based on total financial strength, not just a three-digit score.

Pro Tip: Twelve consecutive months of on-time rent payments, verified in writing by your landlord, carry enormous weight in manual underwriting. If you're planning to apply for cabin financing in the next year, start documenting this now.

The table below shows how manual underwriting compares to automated credit scoring for buyers with weak or no credit:

| Factor | Automated scoring | Manual underwriting |

|---|---|---|

| Primary input | FICO credit score | Income, rent history, bank statements |

| Non-traditional credit accepted | No | Yes (utilities, insurance, rent) |

| Compensating factors considered | Limited | Yes (reserves, down payment, stable job) |

| Best for | Buyers with established credit | Buyers with thin or poor credit files |

| Decision timeline | Minutes | 1 to 5 business days |

FHA manual underwriting guidelines allow approval even with flexible debt-to-income ratios when compensating factors are strong. That means buyers who carry some debt but have stable income, solid rent history, and a few months of savings can still get approved where an automated system would have declined them immediately.

The practical takeaway: if your credit score is low or nonexistent, manual underwriting is not a consolation prize. It's often the better path.

Financing programs that skip the upfront credit inquiry

Beyond manual underwriting, a new category of approval programs offers something genuinely useful for buyers who are unsure whether they'll qualify. These programs review your financial scenario with an actual underwriter before ever pulling your credit.

Mbanc's Clear Approval program is one well-known example. An underwriter reviews your income, assets, and loan scenario within 24 hours of application. No credit pull happens at intake. Only if you choose to proceed after receiving a real scenario does the credit check occur. This approach gives buyers real information without the cost of a hard inquiry.

Who benefits most from programs like this?

- Self-employed buyers with strong income but non-traditional documentation

- Real estate investors using rental income rather than W-2 wages

- Buyers with thin credit files who have strong cash positions

- First-time cabin buyers who want certainty before committing to a full application

Compare this to a conventional pre-approval, where a lender runs your credit, gives you a number, and then conditions everything on further review. The underwriter decision within 48 hours model flips that sequence, giving you a human-reviewed answer before the hard inquiry happens.

For cabin buyers in particular, this matters. Many manufactured cabin purchases fall outside traditional mortgage underwriting because the structure is portable or doesn't sit on a permanent foundation. That makes non-QM lenders and rent-to-own programs especially relevant. Exploring cabin financing options specific to your state gives you a clearer picture of what's available in your market.

What to do before you apply for cabin financing

Preparation is the single most effective thing you can do to improve your approval outcome. Here's a practical sequence to follow:

- Gather your income documents. Pay stubs from the last 30 days, two years of tax returns, and three to six months of bank statements. Self-employed buyers should include profit and loss statements.

- Verify your rent history. Ask your landlord for a letter confirming your payment history. Collect 12 months of canceled checks or bank transfer records as backup.

- Document non-traditional credit. Pull together 12 months of utility bills, insurance statements, and phone bills showing on-time payments.

- Assess your debts. Calculate your total monthly debt payments versus your gross monthly income. Lenders look for manageable ratios.

- Consider a down payment or co-signer. Down payments improve approval odds but don't override other issues. A co-signer with strong credit can strengthen a weak file significantly.

- Research your lender. Check reviews, confirm licensing, and ask directly about when credit checks occur and what fees apply.

Pro Tip: Avoid applying to multiple lenders in rapid succession. Each hard inquiry can lower your credit score. Instead, use programs that review your scenario before pulling credit, or use a broker who submits to multiple lenders through a single inquiry.

Buyers who prepare this way don't need guaranteed approval promises. They come in with documentation strong enough to earn a real yes. You can also review portable building financing approval rates to understand what realistic benchmarks look like in Kentucky and Ohio.

My honest take on guaranteed approval cabin claims

I've seen a lot of buyers come in frustrated, not because they couldn't qualify for financing, but because they spent months chasing claims that were never real. "Guaranteed approval" is a marketing phrase, not a financial product. The moment you stop looking for that promise and start building a file that speaks for itself, the whole process gets easier.

What I've found consistently is this: buyers who show up with documented rent history, six months of bank statements, and a clear picture of their income get approved more often than buyers who focus on finding the "easiest" lender. The documentation is the product you're selling to an underwriter. Make it compelling.

I also think buyers underestimate how much the structure of the purchase matters. A rent-to-own program from a retailer like Ez-cabin operates on completely different criteria than a traditional mortgage. The barrier to entry is lower by design because the retailer holds the risk differently. That's not a loophole. It's a legitimate path that tiny home financing without credit checks has proven works for real buyers.

The buyers I've seen succeed didn't wait for a guaranteed approval. They prepared, asked the right questions, and picked programs that matched their actual situation.

— Team

Get started with Ez-cabin's flexible financing today

Ez-cabin is built for buyers who've been told no before. The rent-to-own program requires only your first month's payment to get started, with no traditional credit check standing between you and your cabin. Buyers across Kentucky and Ohio have used this path to own portable cabins, sheds, garages, and tiny homes without navigating bank loan paperwork.

Whether you shop online or visit one of Ez-cabin's locations in London, KY or Somerset, KY, the process is designed to be fast and transparent. You can browse inventory, configure your structure, and lock in financing in one visit. Explore Ez-cabin's rent-to-own options to see current payment plans, or use the custom cabin builder to design your space before you commit. Most buildings are delivered within one to four weeks.

FAQ

What does "guaranteed approval cabins" actually mean?

The phrase refers to financing programs marketed as accessible to buyers regardless of credit history. No legitimate lender can guarantee approval without reviewing income or repayment ability, so the term is often a marketing claim rather than a true promise.

Do no credit check cabin loans really skip the credit pull?

Not entirely. Most "no credit check" programs defer the credit pull until after an initial scenario review. The credit check happens later in the process, not never. Always ask the lender when the inquiry occurs.

What documents help most for cabin financing with bad credit?

Rent verification, utility payment records, bank statements, and proof of stable income carry the most weight in manual underwriting. Twelve months of on-time rent payments is especially valuable.

Is rent-to-own a legitimate alternative to traditional cabin loans?

Yes. Rent-to-own programs from retailers like Ez-cabin operate outside traditional mortgage underwriting. They typically require only a first month's payment and have more flexible criteria, making them a practical option for buyers with limited or damaged credit.

How long does cabin financing approval typically take?

Traditional loans can take weeks. Manual underwriting decisions run one to five business days. Programs like Mbanc's Clear Approval deliver a real underwriter decision within 24 hours, giving buyers fast clarity without an upfront credit pull.