TL;DR:

- Tiny homes offer significantly higher cash-on-cash ROI and faster payback periods compared to traditional rentals.

- Their demand is driven by short-term vacation rentals and affordable housing needs, especially in Kentucky and Ohio.

Tiny homes generating a 27% cash-on-cash ROI while traditional rentals struggle to crack 10% net margins? That gap is real, and investors across Kentucky and Ohio are starting to notice. The assumption that tiny homes are a fringe lifestyle choice has quietly given way to a more interesting reality: these compact structures can outperform larger properties on a pure cash flow basis. This guide breaks down the financials, logistics, risks, and real-world mechanics of investing in tiny homes for rentals so you can decide whether this market actually fits your portfolio strategy.

Table of Contents

- Understanding the tiny home rental opportunity

- How the numbers actually work: costs, cash flow, and ROI

- Key risks, challenges, and what most investors miss

- How to set up and scale a tiny home rental

- Why tiny homes aren't a one-size-fits-all investment

- Next steps: tiny home solutions for investors

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| High cash returns | Tiny homes offer much higher cash-on-cash returns than traditional rentals due to strong rental demand. |

| Regulatory patchwork | Zoning, permits, and STR rules require careful local research before you invest in Kentucky or Ohio. |

| Hidden costs matter | Delivery, utilities, and insurance expenses can materially affect your investment’s bottom line. |

| Amenities drive profit | Simple upgrades like hot tubs or Wi-Fi can boost nightly rates and occupancy dramatically. |

| Best for active investors | Tiny homes work best for hands-on owners focused on cash flow rather than appreciation. |

Understanding the tiny home rental opportunity

Tiny homes are typically defined as structures under 400 square feet, though many functional rental units fall in the 150 to 300 square foot range. They come in two main forms: units built on wheels (often classified as RVs) and those placed on permanent or semi-permanent foundations. Each has different zoning, financing, and permitting implications that matter enormously once you start looking at real land parcels in Kentucky or Ohio.

The demand driving this market comes from two directions. Short-term rental platforms like Airbnb and VRBO have created a category of travelers specifically seeking unique, intimate experiences over cookie-cutter hotel rooms. Long-term demand is pushed by renters who need affordable housing and are priced out of traditional apartments. Both streams feed into the same tiny home investment thesis.

The Airbnb rental potential in Kentucky and Ohio is particularly strong near recreational areas, state parks, and college towns, where unique accommodations command a premium. Short-term rental yields of $80 to $300 per night with 50 to 75% occupancy translate into monthly revenue between $1,500 and $6,750 per unit. For an affordable cabin investment that costs $40,000 to $80,000 all-in, those numbers change the ROI conversation fast.

Here is a quick market comparison to frame the opportunity:

| Metric | Tiny home rental | Traditional rental |

|---|---|---|

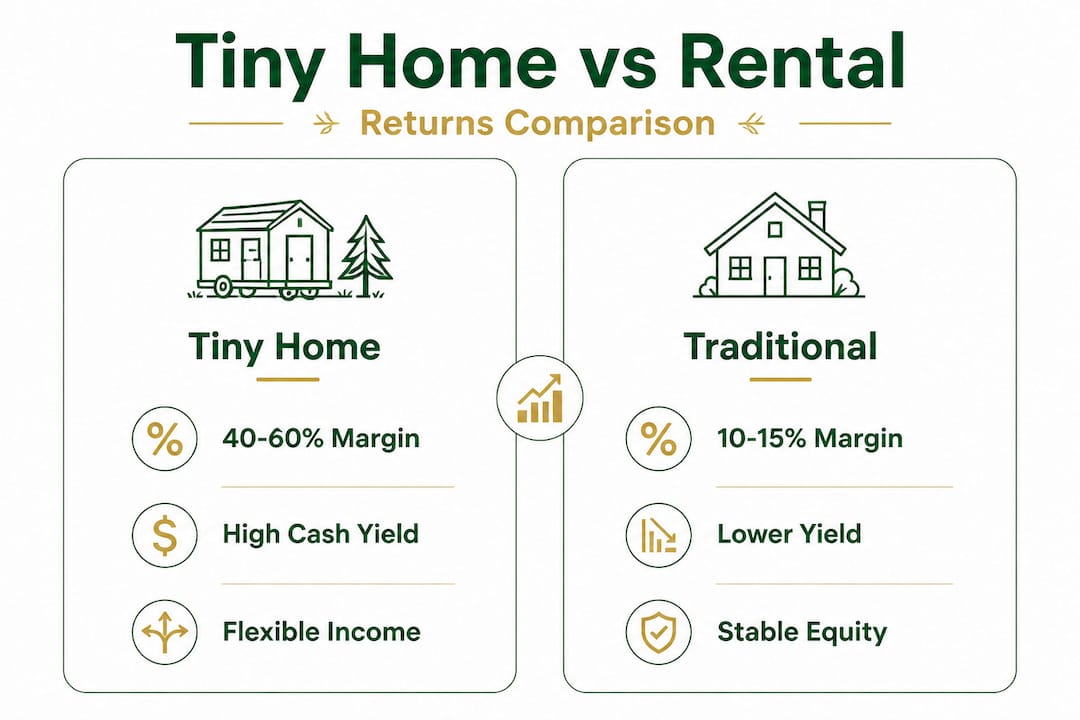

| Net profit margin | 40-60% | 10-15% |

| Cash-on-cash ROI | 25-40% | 6-12% |

| Payback period | 1-5 years | 7-12 years |

| Market growth (CAGR) | 4-13% | 2-4% |

| Monthly revenue range | $1,500-$6,750 | $800-$2,000 |

The tiny home market is growing at 4 to 13% annually, and that trajectory is being shaped by shifting housing preferences, rising construction costs for traditional builds, and a growing appetite for minimalist travel experiences. In both Kentucky and Ohio, rural counties near tourism corridors are seeing new tiny home communities and individual cabin rentals listed and booked consistently.

Key reasons investors look at this market:

- Lower upfront capital compared to purchasing or building a traditional rental property

- Faster deployment, since portable units can often be delivered and set up within weeks

- Flexibility to relocate the unit if one market underperforms

- Niche differentiation on platforms like Airbnb where unique stays command higher rates

How the numbers actually work: costs, cash flow, and ROI

Knowing the top-line revenue potential is a starting point. The real analysis comes from mapping the full cost picture against realistic cash flow projections.

A typical tiny home rental investment breaks down like this:

- Unit purchase or build cost: $25,000 to $70,000 for a quality portable structure

- Land costs: Varies widely; rural Kentucky and Ohio parcels can start at $10,000 to $50,000

- Utility setup: This is often underestimated. Utility connections range from $750 to $25,000 depending on whether you need to run water, electric, and septic from scratch

- Delivery costs: Expect $5,000 to $10,000 for delivery and placement, including any grading or site prep

- Insurance: Higher cost per square foot than a traditional home, so budget accordingly

- Platform and management fees: Typically 15 to 30% of revenue on Airbnb or VRBO if you use a co-host

A practical revenue model: a tiny cabin listed at $150 per night with 60% occupancy generates roughly $2,700 per month. Subtract $500 for platform fees, $200 for insurance, $100 for maintenance reserves, and $300 for utilities, and you are netting around $1,600 per month. Against a total investment of $80,000, that is a 24% annual cash-on-cash return. Compare that to the net margins of 40 to 60% for tiny home rentals versus 10 to 15% for traditional rentals, and the advantage holds up under scrutiny.

Understanding your setup and ongoing costs before you commit to a property is what separates smart acquisitions from expensive lessons.

Pro Tip: Adding one high-value amenity like a hot tub, fire pit, or outdoor shower can meaningfully lift both your nightly rate and your occupancy rate. Guests on Airbnb actively filter for these features, and the added cost is often recovered within two to three months of bookings.

Knowing that tiny home financing options are different from traditional mortgages also affects your cost of capital. More on that shortly, but the short answer is: plan for RV loans, personal loans, or seller financing as your primary tools, not a 30-year conventional mortgage.

Key risks, challenges, and what most investors miss

The cash flow numbers are attractive, but there is a set of risks that trip up investors who skip the homework. These are not deal-breakers, but they are real considerations you need to work through before putting money down.

Zoning and permit complexity is the biggest landmine. There is no unified state framework governing short-term rentals in Kentucky. As described by legal experts tracking the market, Kentucky short-term rentals operate in a "Wild West" regulatory environment where local ordinances govern everything from permits to occupancy limits to tax collection. Some cities like Covington allow short-term rentals in residential zones. Others prohibit them entirely or require specific conditional use permits. Ohio has similar patchwork regulations at the municipal level. You must verify rules with your specific city or county before purchasing land or a unit.

Financing limitations catch many first-time investors off guard. Tiny homes face zoning hurdles and limited financing since traditional mortgage lenders do not treat them as real property, especially units on wheels. RV loans and personal loans are the standard alternatives, typically carrying higher interest rates and shorter repayment terms. This is why understanding your financing hurdles upfront directly affects the profitability model.

Here are the key risks to evaluate before investing:

- Depreciation: Unlike traditional homes, units on wheels depreciate like vehicles. This matters if you are counting on asset appreciation as part of your return

- High management burden for short-term rentals: Turnover between guests means frequent cleaning, restocking, and guest communication. Without systems in place, this becomes a part-time job

- Utility access on rural parcels: Off-grid setups work but add cost and maintenance complexity

- Insurance gaps: Some standard landlord policies exclude structures under a certain square footage or units classified as RVs

"The biggest mistake is treating tiny home investments like a miniaturized version of a standard rental property. The rules, the costs, and the financing landscape are different. Investors who approach it fresh, with their own research for their specific location, tend to do significantly better." This mindset matters especially in Kentucky and Ohio where local variance is high.

Working with a certified builder who understands local requirements can help you sidestep code violations that would otherwise force costly retrofits or, worse, prevent you from listing legally.

Pro Tip: Before you buy land or a unit, call your county planning office directly. Ask specifically about tiny homes or accessory dwelling units (ADUs) on the parcel you are considering. Thirty minutes on the phone can save you from a very expensive mistake.

How to set up and scale a tiny home rental

Once you have done the due diligence, the actual setup process is more straightforward than most investors expect. Here is a practical sequence for getting your first unit income-producing.

-

Choose your land and unit type. Decide early whether you want a unit on wheels (more flexible, financing is harder) or a foundation-placed structure (better for permanent permits). Selecting the right tiny home for your target market matters more than most investors realize. A hiking-trail destination needs different amenities than a college-town rental.

-

Verify zoning and obtain permits. Contact your local planning department. Confirm what is permitted, what inspections are required, and whether short-term rentals are allowed or need a license.

-

Handle utility connections. Plan your water, electric, and sewage before delivery. Rural properties may require a well, septic system, or solar setup. These costs vary enormously and need to be built into your budget from day one.

-

Deliver and set up the unit. Most quality portable buildings are delivered within one to four weeks of purchase. Site prep including a gravel pad or concrete footings should happen before delivery day.

-

Stage and equip for guests. Invest in quality bedding, kitchen basics, and amenities that boost rental value like dedicated outdoor storage, smart locks, and reliable Wi-Fi. These details drive review scores, and review scores drive future bookings.

-

List and price dynamically. Use pricing tools like PriceLabs or Wheelhouse to adjust nightly rates based on local demand, seasonality, and nearby events. Static pricing leaves real money on the table.

The profitability mechanics of rentable tiny homes improve significantly when you scale. Adding a second or third unit to the same parcel spreads land costs, utility infrastructure, and property management time across more revenue-generating doors.

Key amenities that consistently drive higher bookings and rates:

- Hot tubs (can add $25 to $75 per night in premium)

- Fire pits and outdoor seating

- Fast, reliable Wi-Fi

- Pet-friendly features like fenced yards or dog washing stations

- Private parking

Pro Tip: Use dynamic pricing tools from your first month live. Investors who set a flat nightly rate often undercharge during peak weekends and overcharge during slow weekdays. Dynamic tools do this work automatically and typically lift annual revenue by 10 to 20%.

Why tiny homes aren't a one-size-fits-all investment

Here is the perspective that most articles skip: tiny home rentals are genuinely excellent for cash flow, but they are a poor choice for investors who measure success primarily through property appreciation. That distinction matters a lot.

Traditional real estate investors often think in terms of buying low, building equity, and selling at a gain. Tiny homes, particularly units on wheels, do not follow that path. They depreciate over time. The land beneath them may appreciate, but the structure itself often does not hold value the way a stick-built home does. If your exit strategy depends on selling the structure at a profit in five years, you are probably in the wrong asset class.

What tiny homes are genuinely excellent for is high-yield cash flow, particularly through short-term rentals or supplemental income strategies. Investors who treat them as cash-generating tools, not appreciation vehicles, report yields of 25 to 40% cash-on-cash. That is hard to match in traditional real estate without significant leverage.

The regulatory complexity in Kentucky and Ohio also demands that you do your own local homework rather than relying on national averages or blog posts that reference regulations in other states. IRC Appendix Q sets some baseline building standards for tiny homes, but zoning, permitting, and rental licensing are all handled locally. Two counties in Kentucky can have completely different rules, and assuming they match is one of the most common errors new investors make.

Our honest take: the investors who win with tiny home rentals are operationally engaged, locally informed, and focused on cash returns rather than asset growth. If that profile fits you, the numbers are real and the opportunity in Kentucky and Ohio is genuinely underutilized. If you are looking for a passive, set-it-and-forget-it asset, this market will frustrate you.

The niche benefits for storage and short-term rental applications show that tiny structures add versatile income streams beyond just Airbnb bookings, which makes them a more flexible tool in a diversified portfolio.

Next steps: tiny home solutions for investors

Ready to move from research to action? EZ-Cabin works directly with Kentucky and Ohio investors looking to build, customize, and finance portable cabin and tiny home rentals without the friction of traditional dealerships.

You can browse ready-to-deliver units, use our AI-powered customization tools to design your rental space in real time, and lock in financing with no credit check required. Whether you want to secure your building investment with our guaranteed approval financing or build your own cabin tailored to your target rental market, we make the entire process fast and transparent. Explore our financing options to see how little it takes to get started, with only the first month's payment needed upfront and most units delivered within one to four weeks.

Frequently asked questions

What are the main permit and zoning hurdles for tiny homes in Kentucky?

Kentucky has no unified state framework for short-term rentals, so city-specific ordinances govern permits, zoning, and occupancy limits. You must verify rules with your specific local government before purchasing land or listing a rental.

How long does it take to break even on a tiny home rental investment?

Most investors reach ROI payback within 1 to 5 years depending on local demand, pricing strategy, occupancy rates, and the total capital deployed in the investment.

What financing options are available for tiny homes?

Traditional mortgages rarely apply to tiny homes, so investors typically use RV loans, personal loans, or rent-to-own programs as their primary financing tools.

How do amenities affect tiny home rental profits?

Strategic upgrades like a hot tub can boost occupancy by 10% and raise nightly rates by 15 to 25%, making amenities one of the highest-ROI investments you can make after the initial build.