Many buyers assume portable tiny homes qualify for traditional mortgages just like regular houses. That's rarely the case. Size restrictions and foundation requirements exclude most portable tiny homes from conventional loan programs, leaving buyers scrambling for alternatives. This guide clarifies financing options specifically designed for portable tiny homes in Kentucky and Ohio, including no credit check solutions that make ownership accessible regardless of your credit history.

Table of Contents

- Understanding Portable Tiny Homes And Their Financing Challenges

- Why Traditional Mortgages Don't Work For Portable Tiny Homes

- Alternative Financing Options For Portable Tiny Homes

- No Credit Check Financing Mechanisms And Criteria

- Comparison: Rent-To-Own Vs Lease-Purchase Vs Personal Loans

- Common Misconceptions About Portable Tiny Home Financing

- Practical Steps To Secure Portable Tiny Home Financing In Kentucky And Ohio

- Discover Hassle-Free Portable Tiny Home Financing With EZ-Cabin

- Frequently Asked Questions About Portable Tiny Home Financing

Key takeaways

| Point | Details |

|---|---|

| Traditional mortgages exclude portable tiny homes | Most lenders require 400-600 sq ft minimums and permanent foundations, disqualifying portable structures under 400 sq ft. |

| No credit check financing removes barriers | Programs require only first month's payment upfront with flexible 24-72 month terms and no credit verification. |

| Alternative options include personal loans and rent-to-own | Personal loans offer up to $100,000 with fixed terms; rent-to-own provides flexible ownership paths without credit checks. |

| EZ-Cabin streamlines digital financing | Complete the entire process online with guaranteed approval, minimal upfront cost, and delivery within 1-4 weeks. |

| Understanding your credit profile guides choices | Match financing programs to your credit situation and budget for faster approvals and better terms. |

Understanding portable tiny homes and their financing challenges

Portable tiny homes represent a distinct category of housing. These structures typically measure under 400 square feet and many are built on wheels, allowing mobility without requiring permanent foundations. This mobility and compact size make them attractive to buyers seeking affordable, flexible housing options.

However, these same characteristics create financing obstacles. Traditional mortgage lenders generally do not finance tiny homes as they fall below minimum size requirements (usually 400-600 square feet) and lack permanent foundations, rendering many tiny homes ineligible for conventional loans. Lenders view homes without permanent foundations as higher risk investments similar to recreational vehicles rather than real estate.

Key financing challenges for portable tiny homes include:

- Failure to meet lender minimum square footage requirements

- Lack of permanent foundation attachment to land

- Classification as personal property rather than real estate

- Limited comparable sales data for appraisal purposes

- Restricted insurance coverage options for non-traditional structures

These barriers force buyers to explore alternative financing options for tiny houses beyond traditional mortgage channels. Understanding why conventional loans don't work helps you identify suitable financing paths from the start.

Why traditional mortgages don't work for portable tiny homes

Mortgage lenders operate within strict guidelines that protect their investments. These requirements systematically exclude portable tiny homes from eligibility, regardless of the buyer's creditworthiness or down payment capacity.

Mortgage lenders require permanent foundations and minimum loan amounts ($50,000+), while tiny homes often have loan needs below lender minimums and lack property insurance options. Most conventional mortgage programs set minimum loan thresholds between $50,000 and $75,000 because processing costs remain similar regardless of loan size. Tiny homes frequently cost less than these minimums, making them unprofitable for traditional lenders to finance.

Additional mortgage barriers include:

- Permanent foundation requirements that portable structures cannot meet

- Minimum home size policies typically starting at 400 square feet

- Property insurance mandates that insurers won't cover for mobile structures

- Appraisal standards requiring comparable home sales in the same area

- Underwriting guidelines classifying tiny homes as specialty properties

"Lenders see portable tiny homes as personal property like RVs or boats rather than real estate. This classification shifts financing entirely away from mortgage products to vehicle loans or unsecured personal loans."

These mortgage lender restrictions aren't arbitrary. They reflect risk management policies and regulatory frameworks designed for traditional real estate. The good news is that alternative financing mechanisms specifically address portable tiny home purchases.

Alternative financing options for portable tiny homes

When traditional mortgages fail, several financing alternatives fill the gap for portable tiny home buyers. These options recognize the unique nature of tiny homes and provide flexible terms suited to their lower price points and non-traditional status.

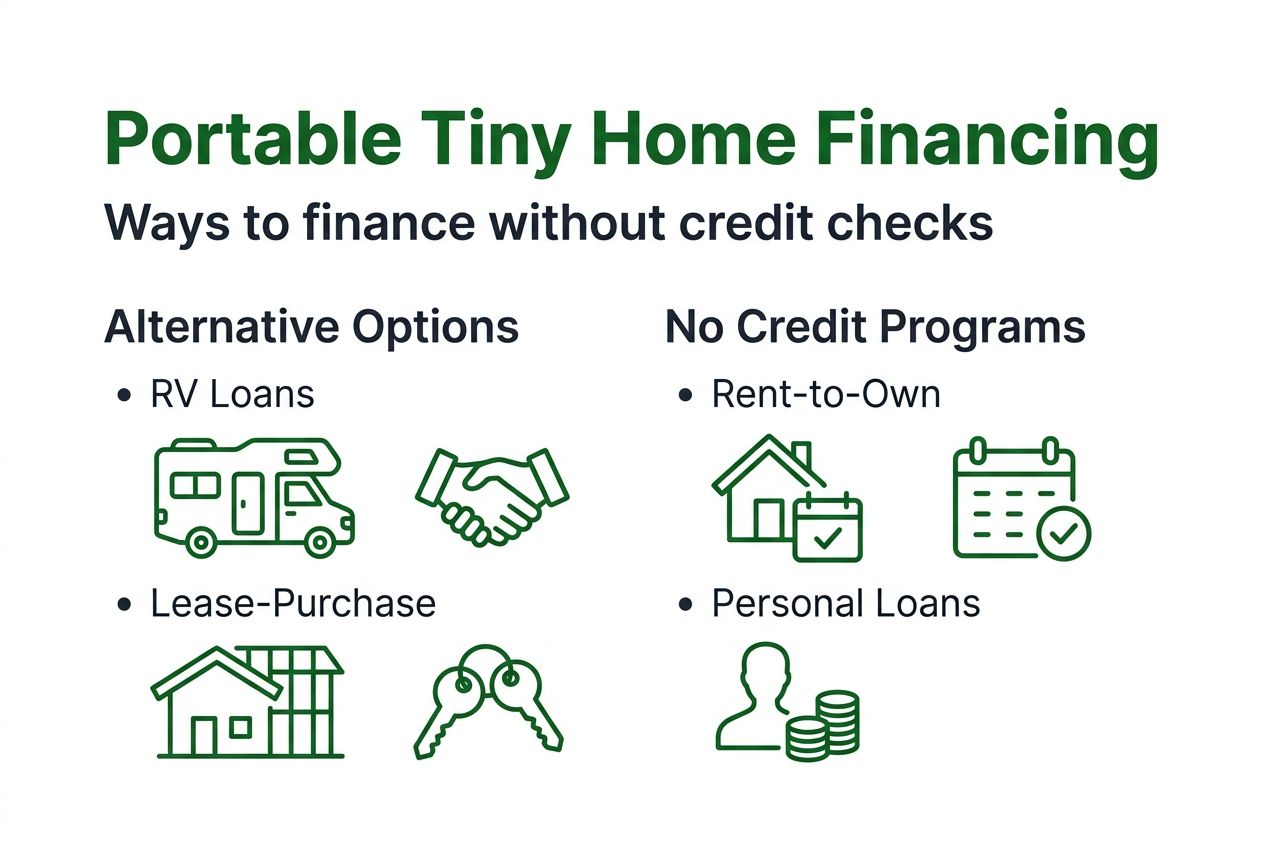

Many alternative financing options for tiny homes circumvent traditional mortgages, including RV loans, peer-to-peer lending, manufacturer financing, and crowdfunding. Each approach offers distinct advantages depending on your credit profile and purchase timeline.

Personal loans offer flexible amounts up to $100,000 and terms up to 60 months, providing fast and flexible financing without collateral requirements. Banks and online lenders evaluate your credit score and income to determine eligibility and interest rates, typically ranging from 6% to 36% APR.

Popular alternative financing options include:

- Personal unsecured loans from banks or online lenders

- RV loans for RVIA-certified tiny homes on wheels

- Peer-to-peer lending platforms connecting borrowers with individual investors

- Manufacturer or dealer financing programs like EZ-Cabin financing

- Rent-to-own agreements with gradual equity buildup

- Lease-purchase arrangements with end-of-term purchase options

These pathways provide access regardless of whether your tiny home qualifies as real estate. Personal loans work particularly well for buyers with good credit who can secure favorable interest rates, while rent-to-own models serve those who need more flexible qualification criteria.

No credit check financing mechanisms and criteria

No credit check financing removes the most common barrier to tiny home ownership: credit qualification. These programs evaluate ability to pay based on income verification rather than credit history, opening doors for buyers with past financial challenges or limited credit profiles.

No credit check financing typically requires minimal down payment (around 20%), some models require only first month's payment upfront, and terms typically range from 24 to 72 months with flexible monthly payments. This structure makes ownership immediately accessible without waiting to rebuild credit scores.

Typical no credit check financing criteria include:

- Proof of steady income or employment

- Valid government-issued identification

- Bank account for automatic payment processing

- Down payment ranging from first month's payment to 20% of purchase price

- Residency verification in the service area

The application process follows these streamlined steps:

- Select your portable tiny home model and customize features

- Complete a brief online application with income verification

- Receive instant or same-day approval notification

- Make your initial payment to secure the unit

- Schedule delivery within 1-4 weeks

Pro Tip: Even with no credit check programs, maintaining consistent payment records helps you qualify for better financing terms on future purchases and builds positive payment history.

EZ-Cabin no credit check financing exemplifies this model. Buyers need only the first month's payment to start, receive guaranteed approval without credit verification, and complete the entire transaction digitally from browsing to delivery scheduling.

Comparison: rent-to-own vs lease-purchase vs personal loans

Choosing between financing options requires understanding how each structure affects your payments, ownership timeline, and total cost. This comparison clarifies the practical differences.

| Feature | Rent-to-Own | Lease-Purchase | Personal Loans |

|---|---|---|---|

| Credit Check | None required | Rarely required | Always required |

| Initial Payment | First and last month | First month plus deposit | Down payment or none |

| Monthly Payments | Fixed rental payments | Fixed lease payments | Fixed loan payments |

| Ownership Timeline | Gradual equity buildup | Purchase option at end | Immediate ownership |

| Early Payoff | Often allowed | Contract specific | Usually allowed |

| Total Cost | Higher due to interest equivalent | Moderate, depends on purchase price | Lower with good credit rates |

| Term Flexibility | Very flexible | Moderate flexibility | Fixed term length |

| Default Consequences | Return unit, lose equity | Return unit, lose payments | Credit damage, potential collections |

Rent-to-own requires first and last month payments upfront with no credit verification. You make monthly payments over 24-72 months, gradually building ownership equity. Many programs, including rent-to-own financing, allow early payoff to reduce total cost.

Lease-purchase agreements function similarly but typically include a balloon payment or purchase option at lease end rather than automatic ownership progression. This structure provides flexibility if your plans change.

Personal loans require credit checks and provide immediate ownership through lump sum disbursement. You repay with fixed monthly installments at interest rates determined by your credit score. Good credit (700+) can secure rates below 10%, making personal loans cost effective despite requiring credit qualification.

Key considerations:

- Choose rent-to-own if you need guaranteed approval regardless of credit

- Consider lease-purchase if you want flexibility before committing to ownership

- Opt for personal loans if you have good credit and want immediate ownership

- Calculate total cost including interest or rent premiums before deciding

Common misconceptions about portable tiny home financing

Misunderstandings about tiny home financing prevent many buyers from exploring viable options. Correcting these misconceptions opens paths to ownership that buyers might otherwise dismiss.

Tiny homes usually cannot secure traditional mortgages due to size and foundation requirements. Most buyers assume mortgages represent the only legitimate financing path, causing them to abandon their tiny home search prematurely. In reality, alternative financing mechanisms provide equally valid ownership routes.

Common false beliefs include:

- All financing requires excellent credit scores (many programs skip credit checks entirely)

- Large down payments are mandatory (some require only first month's payment)

- Financing takes months to arrange (digital platforms provide same-day approvals)

- Only new tiny homes qualify for financing (used units can be financed through personal loans)

- Rent-to-own means you never truly own (contracts transfer full ownership upon completion)

Credit checks are often not mandatory for many financing options. Programs specifically designed for portable buildings recognize that credit scores don't always reflect current ability to pay. Income verification and payment history matter more than past credit challenges.

Pro Tip: Don't assume you won't qualify based on past credit issues. Apply to no credit check programs first to establish baseline approval, then compare terms with credit-based options if you want to explore all possibilities.

Educating yourself about actual requirements and available programs prevents financing delays. Many buyers waste months trying to secure traditional mortgages when alternative options would provide faster, more accessible ownership paths.

Practical steps to secure portable tiny home financing in Kentucky and Ohio

Taking action on portable tiny home financing requires a strategic approach. These steps guide you from initial assessment through final purchase.

-

Evaluate your credit and financial situation honestly. Check your credit score and review your budget to understand monthly payment capacity. This assessment determines which financing programs best match your profile.

-

Research Kentucky and Ohio financing providers specializing in portable buildings. Focus on programs offering EZ-Cabin financing terms suited to tiny homes, including no credit check options and low initial payments.

-

Compare total costs across financing methods. Calculate total amount paid over the financing term, including interest or premium pricing, to identify the most cost effective option.

-

Prepare required documentation including proof of income, identification, and bank account information. Having documents ready speeds approval processes significantly.

-

Use digital financing tools to customize your tiny home, apply for financing, and schedule delivery in one integrated workflow. Modern platforms eliminate multiple site visits and paperwork delays.

-

Review contract terms carefully before signing. Understand payment schedules, early payoff options, default consequences, and ownership transfer conditions.

-

Arrange site preparation and utility connections before delivery. Coordinate with delivery teams to ensure your property is ready for tiny home placement.

Pro Tip: Start your financing application during business days early in the week. This timing ensures faster response to any verification questions and can expedite approval by several days compared to weekend applications.

Choose providers offering integrated services from financing through delivery. Companies like EZ-Cabin streamline the entire process, reducing coordination headaches and accelerating your ownership timeline. Most buyers complete purchases within 2-4 weeks using digital platforms.

Discover hassle-free portable tiny home financing with EZ-Cabin

Applying the financing knowledge you've gained becomes simple with the right partner. EZ-Cabin specializes in removing traditional financing barriers for Kentucky and Ohio buyers seeking portable cabins, tiny homes, sheds, and garages.

We provide guaranteed approval with no credit checks required, making ownership accessible regardless of your credit history. You need only the first month's payment to start, eliminating large down payment obstacles that delay other financing methods.

Our fully digital process lets you browse inventory, customize your building with AI-powered design tools, secure EZ-Cabin financing options, and schedule delivery without visiting a physical location. Most customers complete purchases within 1-4 weeks from initial browsing to delivery.

Explore our selection of portable cabins and buildings shop offerings tailored to Kentucky and Ohio needs. Visit EZ-Cabin locations near you in London, KY or Somerset, KY if you prefer seeing buildings in person before purchasing. Either way, our streamlined financing makes your tiny home dream achievable today.

Frequently asked questions about portable tiny home financing

Do I need good credit to finance a portable tiny home?

No, many financing options including rent-to-own and programs like EZ-Cabin require no credit check at all. These programs evaluate your ability to pay based on current income rather than past credit history, making approval accessible regardless of your credit score.

What down payment do I need for tiny home financing?

Down payment requirements vary by program, ranging from just the first month's payment to around 20% of the purchase price. No credit check financing typically requires minimal upfront payments, often just first and last month, making ownership immediately affordable for most buyers.

How long are typical financing terms for portable tiny homes?

Financing terms typically range from 24 to 72 months depending on the program and purchase price. Rent-to-own agreements often offer 36-60 month terms with flexible early payoff options, while personal loans may extend up to 60 months with fixed payment schedules.

How does rent-to-own differ from getting a personal loan?

Rent-to-own requires no credit check and structures payments as rental installments with gradual equity buildup, while personal loans require credit approval and provide immediate ownership through lump sum disbursement. Rent-to-own typically costs more over time but offers guaranteed approval, whereas personal loans provide lower costs for buyers with good credit.

How quickly can I get approved and take delivery in Kentucky or Ohio?

Approval through no credit check programs often happens within 24 hours of application submission. Once approved and you make your initial payment, delivery typically occurs within 1-4 weeks depending on your selected model's availability and site preparation requirements. Digital platforms expedite the entire timeline significantly compared to traditional financing routes.

Can I finance a used portable tiny home?

Yes, though options differ from new unit financing. Personal loans work well for used tiny homes since they provide lump sum payments directly to sellers. Some specialized lenders and rent-to-own programs also accept quality used units, though terms and rates may vary based on the structure's age and condition.