TL;DR:

- Modern financing options make owning a cabin or tiny home accessible without requiring large savings or perfect credit.

- Buyers can start building equity immediately through various loans or rent-to-own programs tailored to their financial situations.

- Understanding the total cost, loan type differences, and negotiating terms helps ensure a smart, affordable purchase aligned with long-term goals.

Most people assume that owning a cabin or tiny home means either having a large pile of savings or a spotless credit score. That assumption stops a lot of Kentucky and Ohio families from ever exploring what's actually possible. The reality is that modern financing has completely changed the picture. Whether you're looking at a cozy retreat on rural land, a backyard studio, or a full-time tiny home, today's financing tools make it far easier to get into a quality building without waiting years to save up. This guide breaks down how financing works, compares the main options, and gives you practical steps to move forward.

Table of Contents

- Why financing matters when buying a cabin

- Main financing options for cabins and tiny homes

- Chattel loans vs. traditional mortgages: What Kentucky and Ohio buyers need to know

- Rent-to-own and credit-friendly solutions for Kentucky and Ohio residents

- What most cabin buyers miss about smart financing

- Discover credit-friendly financing with EZ-Cabin

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Financing expands access | The right financing makes owning a cabin, shed, or tiny home affordable for more Kentucky and Ohio buyers. |

| Know your loan options | Chattel, rent-to-own, and mortgages each have unique pros, cons, and requirements. |

| Read the fine print | Understanding terms and total costs is essential to avoid costly mistakes and regrets. |

| Credit-friendly solutions exist | Even buyers with low credit or little savings can find suitable cabin financing options. |

Why financing matters when buying a cabin

Most buyers in Kentucky and Ohio picture cabin ownership as something they'll pursue "someday," once they've saved enough. But financing flips that thinking on its head. Instead of waiting years to accumulate enough cash, you can start building equity in a structure today while spreading the cost over manageable monthly payments.

Think about what that actually means in practice. A well-built modern cabin might cost $15,000 to $40,000 or more, depending on size and features. Very few families have that sitting in a savings account. Financing turns that large upfront number into a payment that fits inside a real monthly budget. And because you're financing, you don't have to settle for a basic box. You can choose financing solutions for prefab cabins that let you add custom windows, upgraded siding, insulation packages, and more.

Here's why financing decisions go far beyond just "getting approved":

- Total cost of ownership: Your interest rate and loan term determine how much you actually pay over time, sometimes much more than the purchase price.

- Customization access: With financing, you can afford a build that truly fits your needs rather than settling for whatever fits a cash budget.

- Purchase experience: Programs without complicated approvals reduce stress and let you focus on getting the right building.

- Credit impact: Some options report positively to credit bureaus, while others don't. That matters for your financial future.

- Down payment flexibility: Credit-friendly plans often require little to nothing upfront, which is a game-changer for buyers with tight liquidity.

Understanding the financing impact in Kentucky and Ohio is especially relevant here because rural property values, land ownership patterns, and local income levels all shape which financing tools make the most sense.

"The right financing option isn't the one with the lowest payment — it's the one that fits your full financial picture, including total cost, term length, and what happens if your situation changes."

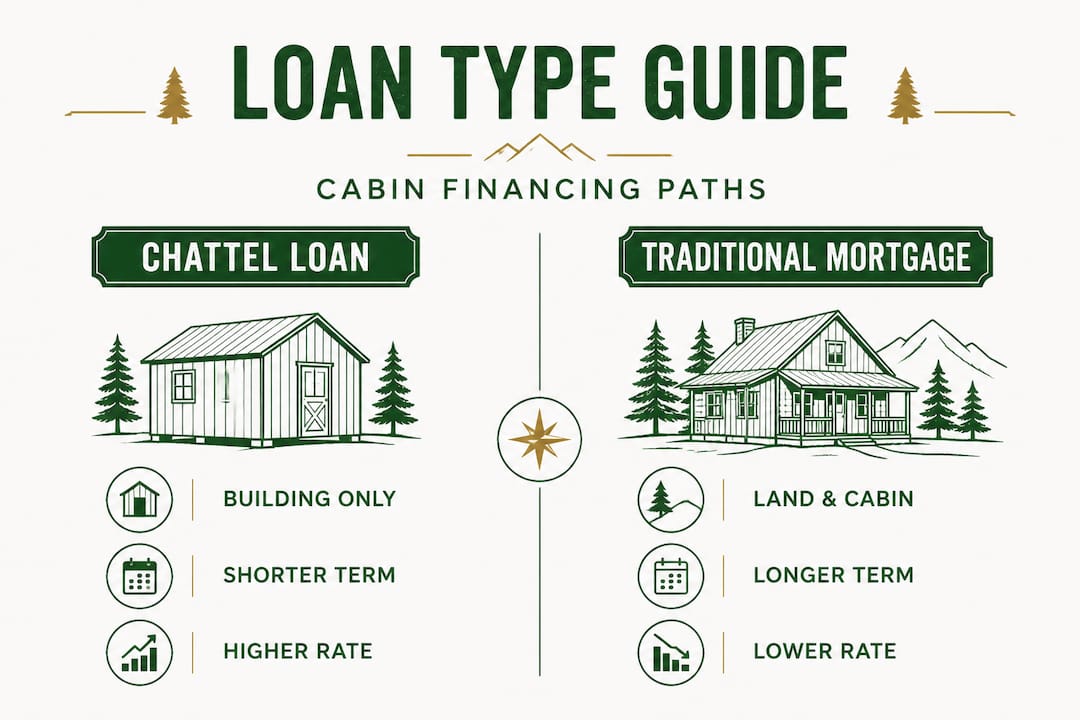

One often-overlooked detail: chattel mortgages are commonly used when the land is not being purchased along with the cabin. These loans treat the building as personal property rather than real estate, and they tend to carry higher interest rates, shorter terms, and fewer consumer protections than a standard mortgage. Knowing this upfront keeps you from being surprised later.

Main financing options for cabins and tiny homes

Understanding why financing matters, let's break down the main ways buyers can finance a new cabin or tiny home.

There are three primary paths most buyers in Kentucky and Ohio will consider: chattel loans, personal loans, and rent-to-own programs. Each one has a different structure, different eligibility requirements, and different tradeoffs.

| Option | Credit requirement | Down payment | Ownership timeline | Best for |

|---|---|---|---|---|

| Chattel loan | Moderate to good | 5% to 20% | Immediate | Buyers with land |

| Personal loan | Good to excellent | None required | Immediate | Smaller purchases |

| Rent-to-own | None or minimal | First payment only | End of contract | Buyers without credit |

Chattel loans are tied directly to the structure itself, not the land underneath it. Because the building is the collateral, lenders see more risk, and that risk gets passed to the buyer through higher interest rates. The chattel mortgage structure typically offers shorter repayment terms (often 15 to 20 years instead of 30), fewer legal protections if something goes wrong, and in some cases, stricter default consequences.

Personal loans work differently. You borrow a fixed amount, pay it back over a set term, and the cabin itself isn't collateral. That flexibility is appealing, but personal loans usually require strong credit and have lower borrowing limits. They work well for smaller sheds or basic cabins but may fall short for larger or fully custom builds.

Rent-to-own is the most accessible option for buyers with limited savings or credit challenges. You pay a set monthly amount with an option to own the building at the end of the contract. Many programs don't require a credit check at all, and checking portable building financing approval rates shows just how accessible these programs have become in recent years. There are also alternative financing options worth comparing if one path doesn't feel right.

Key advantages and disadvantages across all options:

- Chattel loans offer real ownership from day one but cost more in interest long-term

- Personal loans are flexible but credit-dependent and limited in size

- Rent-to-own gets you into a building with almost no barrier but typically costs more overall

Pro Tip: If you don't own the land where the cabin will sit, rent-to-own or a personal loan will likely serve you better than a chattel loan, since chattel loans are mainly designed for buyers who have a permanent site for the structure.

Chattel loans vs. traditional mortgages: What Kentucky and Ohio buyers need to know

Now that you've seen the main options, let's take a closer look at chattel loans and traditional mortgages, since these are common and commonly misunderstood by local buyers.

The single biggest difference is what the loan is secured against. A traditional mortgage uses both the land and the structure as collateral. A chattel loan only uses the structure. That distinction drives nearly every other difference between the two.

| Feature | Chattel loan | Traditional mortgage |

|---|---|---|

| Collateral | Building only | Land plus building |

| Typical interest rate | Higher (often 6% to 14%) | Lower (often 4% to 7%) |

| Loan term | 15 to 20 years | 15 to 30 years |

| Consumer protections | Fewer | More (federal/state laws) |

| Approval speed | Faster | Slower |

| Credit requirement | Moderate | Good to excellent |

Because chattel loans carry higher rates and shorter terms, monthly payments on a chattel loan can be significantly higher than on a comparable traditional mortgage for the same purchase price. For example, a $30,000 chattel loan at 10% over 15 years produces a much higher monthly payment and total interest paid than the same amount financed at 5% over 30 years through a traditional mortgage.

Here's a real-world scenario many Kentucky buyers face. You've found a piece of rural property, or maybe you're placing a cabin on family land. You don't need a land purchase, just the building. That automatically puts you into chattel or personal loan territory, since there's no real estate transaction for a traditional mortgage to attach to. This is why understanding the specifics before you shop matters so much. Planning ahead, including looking into affordable cabin delivery options, helps you see the total picture clearly.

Pro Tip: If you're comparing loan offers, ask each lender for the total repayment amount over the full term, not just the monthly payment. A lower monthly payment with a longer term often means thousands more paid overall.

Traditional mortgages offer meaningful protections: regulated disclosures, defined foreclosure timelines, and federal consumer laws that apply during the lending process. Chattel loans, by contrast, are governed more loosely, which is why reading every line of a chattel agreement before signing matters enormously.

Rent-to-own and credit-friendly solutions for Kentucky and Ohio residents

If the usual financing options still feel out of reach, don't worry. Rent-to-own and other flexible plans make it possible for more people to get into a quality cabin without the traditional barriers.

Rent-to-own programs have grown significantly in the portable building space. Here's how the process typically works:

- Select your building. Browse available models or customize one to your specifications. Some providers let you adjust size, color, doors, windows, and interior layout before committing.

- Submit a basic application. Most rent-to-own programs ask only for proof of income and a valid ID. No credit check, no hard inquiry on your report.

- Make your first payment. Most programs require only the first month's payment to get started, which is typically a fraction of the total building price.

- Take delivery. Your building arrives and gets set up at your location, often within one to four weeks of approval.

- Pay monthly and build toward ownership. Each payment moves you closer to owning the building outright. At the end of the contract, you own it.

- Early payoff option. Many programs offer discounts if you pay off the balance before the term ends, which reduces the higher overall cost associated with rent-to-own.

There are a few terms to watch for. Rent-to-own contracts can include clauses about missed payments, late fees, and repossession timelines that are worth reading carefully. Total cost is also higher than a straight purchase, since the convenience and accessibility come with a price premium. Understanding that tradeoff helps you make a clear-eyed decision. For buyers thinking long-term, investing in customized, affordable cabin options through rent-to-own can still deliver strong value, especially if the building increases in utility or resale appeal through personalization. The key is comparing the total amount you'll pay against what the building is worth to you in use and enjoyment.

That said, chattel loan risks and rent-to-own costs both pale in comparison to the cost of waiting indefinitely to save up cash. For most buyers, the real risk is inaction.

Pro Tip: If you want a customized cabin but are using rent-to-own, finalize your layout and upgrades before the contract is signed. Changing features mid-contract can be complicated and may affect your payment terms.

What most cabin buyers miss about smart financing

Here's some real talk most articles skip over. Buyers obsess over getting approved, and then forget to ask whether the deal they got approved for actually makes sense.

We've seen this pattern repeatedly: a buyer falls completely in love with a cabin model before checking their budget or reading through payment scenarios. Emotion drives the decision, and they sign a financing agreement without understanding the total repayment, what happens if they miss a payment, or whether the term length fits their realistic income outlook. The cabin investment insights most buyers need aren't complex, but they do require slowing down before signing anything.

The most overlooked factor is total cost. Not the monthly payment. Not the interest rate. The total amount you will pay from the first payment to the last. Once you see that number, you can make a genuinely informed decision about whether to accept shorter terms with higher payments to reduce total interest, or whether a longer, lower-payment plan fits your cash flow better.

Negotiating terms is also an underused skill. Many buyers assume the terms presented to them are fixed. They often aren't. Asking for a lower rate, a shorter term, or a different payment schedule costs nothing and sometimes works. Providers want to close deals. If you come in knowing the market rates and asking intelligent questions, you're more likely to get a better deal than someone who just says yes to the first offer.

The emotional pitfall is real. Buying a cabin has genuine excitement attached to it, especially when you can see it customized and visualized in real time. That excitement is not a bad thing, but it becomes a problem when it overrides practical judgment. Set your budget ceiling before you start browsing. Stick to it.

Discover credit-friendly financing with EZ-Cabin

If you're ready to see what financing can do for your cabin goals, EZ-Cabin is built exactly for Kentucky and Ohio buyers who want quality without complicated approvals or hidden fees.

EZ-Cabin specializes in rent-to-own and low-barrier financing with guaranteed approval and no credit check required. You only need your first month's payment to get started, and most buildings are delivered within one to four weeks. Our AI-powered tools let you design your cabin in real time before you commit, so you know exactly what you're getting. Explore flexible financing options tailored to your budget, build your own cabin using our customization tools, or browse available buildings ready for fast delivery across Kentucky and Ohio. No dealership pressure. No confusing paperwork. Just a straightforward path to the building you want.

Frequently asked questions

What credit score do I need to finance a cabin in Kentucky or Ohio?

Many rent-to-own and chattel loan programs do not require a high credit score, so buyers with less-than-perfect or even no credit history can still qualify for cabin financing.

Are rent-to-own cabins more expensive than traditional loans?

Yes, rent-to-own typically costs more overall because of higher effective rates and shorter terms, but it's far more accessible than most traditional financing options for buyers without strong credit.

Can I customize a cabin if I use financing?

Most rent-to-own and financing programs allow customization within your approved budget, so you can often adjust colors, windows, doors, and layout before your contract is finalized.

Is a down payment always required for cabin financing?

Not always. Many credit-friendly and rent-to-own plans require only the first month's payment to get started, with no traditional down payment needed at all.

What is the biggest risk with chattel loans?

The biggest risk is that chattel loans carry higher rates and fewer consumer protections than traditional mortgages, especially if you don't own the land where the cabin is placed.