Most buyers in Kentucky and Ohio assume financing a prefab cabin, office, or storage building is a complicated, uphill battle. That assumption is wrong, and it's costing people real money. Prefab homes in rural areas can qualify for standard and government-backed loans, breaking the myth that financing is difficult or unavailable. Whether you're a first-time homebuyer looking for an affordable cabin or an investor adding storage units to your portfolio, flexible loan products exist specifically for your situation. This guide walks you through every major financing path, what affects your approval odds, and how to make the smartest move for your budget.

Table of Contents

- What makes prefab building financing unique?

- Types of prefab buildings and how they affect financing

- Core financing options for prefab buildings in Kentucky and Ohio

- How financing impacts costs and investment returns

- Tips for choosing the right financing path

- Explore flexible prefab building financing with EZ-Cabin

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Flexible loan options | Prefab buildings qualify for a wide range of financing, from standard mortgages to government-backed programs. |

| Building type matters | The kind of prefab structure and its foundation affect which loans you can get and at what rates. |

| Big cost savings | Modular and manufactured homes can cost tens of thousands less than traditional construction in Kentucky and Ohio. |

| Rural buyers advantage | Special USDA loans in Kentucky and Ohio make prefab ownership achievable with low down payments. |

| Preparation pays off | Knowing your building type, land status, and loan requirements leads to fast, affordable prefab financing. |

What makes prefab building financing unique?

Prefab financing isn't complicated once you understand why it works differently from a traditional home loan. The core difference comes down to how and where the building is constructed. With a site-built home, the lender can easily assess value at every stage of construction. With a prefab structure, the building is assembled in a factory and delivered to your land, which changes how lenders evaluate risk.

That said, your options are broader than most people realize. Here's what shapes your financing path:

- Foundation type: A prefab on a permanent foundation opens the door to conventional mortgages, FHA, VA, and USDA loans.

- Building purpose: Primary residences, investment properties, and non-residential structures each attract different loan products.

- Building classification: Modular, manufactured, and portable structures are treated differently by lenders.

- Land ownership: Owning the land where the building sits strengthens your application significantly.

The single biggest factor is foundation. Modular prefab homes on permanent foundations qualify for standard mortgages including conventional, FHA, VA, and USDA options. That's the same menu of loans available for a traditionally built house. If your structure sits on a non-permanent foundation, you'll likely look at chattel loans or rent-to-own plans instead.

Pro Tip: Before you apply for any loan, confirm whether your planned building site allows a permanent foundation. That one detail can unlock significantly better interest rates and loan terms.

For buyers exploring affordable portable building options in Kentucky and Ohio, understanding this distinction early saves time and prevents surprises during the application process. Offsite construction genuinely requires a unique lender approach, but that doesn't mean fewer choices. It means knowing which door to knock on.

Types of prefab buildings and how they affect financing

Not all prefab buildings are created equal in the eyes of a lender. The type of structure you choose directly affects which loans you can access, your approval odds, and your total cost.

Here's a quick comparison to orient you:

| Building type | Built to | Foundation | Best loan options |

|---|---|---|---|

| Modular home | Local building code | Permanent | Conventional, FHA, VA, USDA |

| Manufactured home | HUD code | Permanent or chassis | FHA, USDA, chattel |

| Portable/storage building | Varies | Non-permanent | Rent-to-own, personal loan |

| Prefab cabin | Varies | Permanent or skids | Rent-to-own, personal, some FHA |

As the comparison of manufactured vs modular shows, the distinction between HUD-code manufactured homes and locally coded modular homes is critical. A modular home on a permanent foundation is treated almost identically to a site-built home by most lenders. A manufactured home on a chassis is a different story.

Key differences that affect your loan:

- Code compliance: Modular homes meet local and state codes; manufactured homes meet federal HUD standards.

- Foundation permanence: Permanent foundations qualify for more loan types and lower rates.

- Lender risk perception: Structures that can be moved carry higher perceived risk, which raises rates.

- Resale value: Modular homes on permanent foundations appreciate more like traditional homes.

"The type of foundation your prefab sits on is often the single biggest factor in determining which loans are available to you and at what rate."

For investors, customizable cabins and storage units that don't require permanent foundations are often best financed through rent-to-own dealer programs. These plans skip the traditional credit check process entirely, making them accessible for buyers who don't qualify for conventional loans. The [modular garage benefits](https://www.blog.ez-cabin.com/blog/why-buy-modular garages affordable fast customizable/) for investors are also worth reviewing if you're adding functional structures to a property.

Understanding modular vs traditional costs helps you frame the financing conversation correctly from the start.

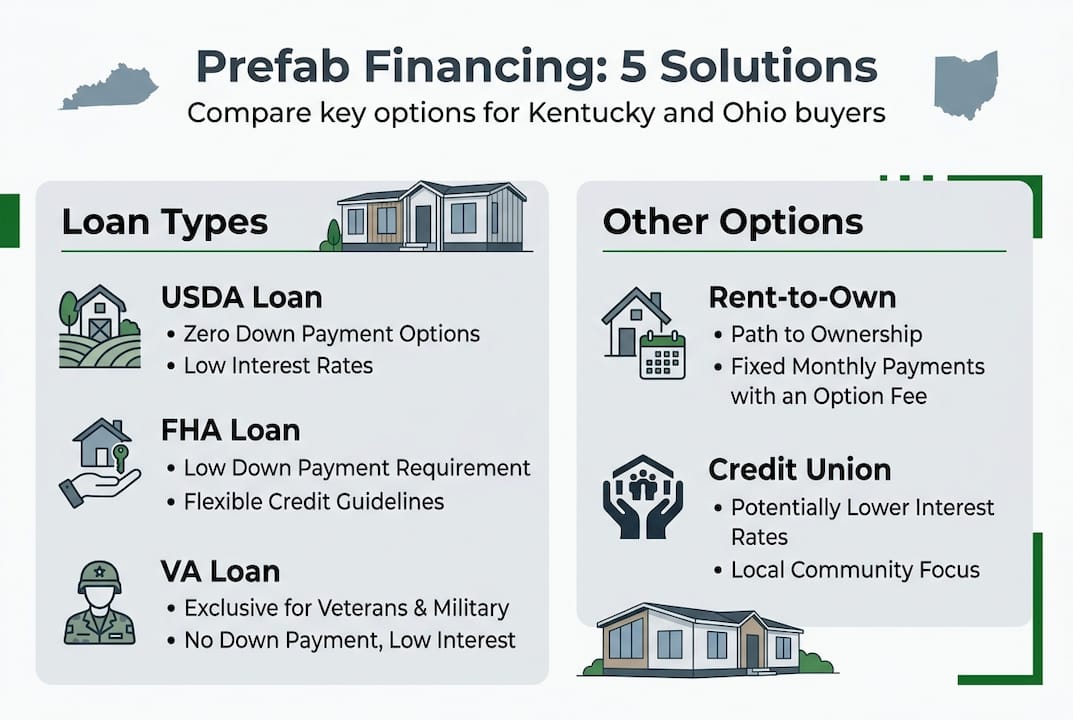

Core financing options for prefab buildings in Kentucky and Ohio

Kentucky and Ohio buyers have access to a strong lineup of loan products. Here's what's on the table in 2026:

| Loan type | Down payment | Credit score | Best for |

|---|---|---|---|

| USDA Rural | 0% | 640+ | Rural prefab homes, 400 sq ft+ |

| FHA | 3.5% | 580+ | Manufactured and modular homes |

| VA | 0% | Varies | Eligible veterans, modular homes |

| Conventional | 5-20% | 620+ | Modular on permanent foundation |

| Chattel loan | 5-20% | 575+ | Manufactured on chassis |

| Rent-to-own | First month only | None required | Portables, cabins, storage |

The standout option for rural buyers is the USDA loan. USDA supports 100% financing for rural prefab and manufactured homes in Kentucky and Ohio, provided you have a 640+ credit score, a permanent foundation, and a structure of at least 400 square feet. That means zero down payment for eligible buyers, which is a major advantage.

Here's how to qualify, step by step:

- Confirm rural eligibility: Use the USDA's online map to verify your property address qualifies.

- Check your credit score: Most government-backed loans require 580 to 640 minimum.

- Verify foundation type: Permanent foundation is required for USDA and most FHA loans.

- Gather income documentation: Lenders need two years of tax returns and recent pay stubs.

- Get a written building estimate: Lenders want to see total project costs, including site prep.

Pro Tip: USDA loans are one of the most overlooked financing tools for prefab buyers in rural Kentucky and Ohio. Many buyers assume they won't qualify, but large portions of both states fall within USDA-eligible zones. Check before you assume.

For buyers who don't qualify for government-backed loans, tiny home financing tips and garage financing without credit checks offer practical alternatives. Rent-to-own plans from dealers like EZ-Cabin require only the first month's payment to get started, with no credit check required. More details on USDA prefab loans are available if you want to dig into the specifics.

How financing impacts costs and investment returns

Choosing the right loan isn't just about getting approved. It's about what you pay over time and how quickly you see a return if you're investing.

Prefab modular homes can save buyers $60,000 to $80,000 compared to traditional site-built construction, and monthly payments can run $150 to $350 lower. That's a meaningful difference over a 15 or 30-year loan term. For investors, lower build costs mean faster break-even on rental income.

Here's how financing structure affects your bottom line:

- Lower purchase price means a smaller loan principal and less interest paid over time.

- Zero-down USDA loans preserve cash for site prep, utilities, and upgrades.

- Rent-to-own plans eliminate upfront financing costs but may carry higher total payments.

- Shorter build timelines (often 4 to 12 weeks for prefab) mean rental income starts sooner for investors.

- Chattel loans carry higher interest rates than mortgage products, increasing long-term cost.

For investors specifically, the speed advantage of prefab is a real financial benefit. A site-built structure might take 6 to 12 months. A prefab cabin or storage unit can be delivered and generating rental income within weeks. That faster timeline directly improves your return on investment.

Pro Tip: When calculating your total financing need, don't forget site preparation costs. Grading, utility hookups, and foundation work can add $5,000 to $20,000 to your project. Build that into your loan request from the start to avoid a funding gap mid-project.

For a deeper look at numbers, prefab cost insights and prefab shed cost benefits break down real figures for Kentucky and Ohio buyers. The full cost breakdown is also worth reviewing before you finalize your budget.

Tips for choosing the right financing path

Knowing your options is one thing. Choosing the right one for your specific situation is where most buyers stumble. Here's how to get it right.

Step-by-step preparation for loan approval:

- Know your building type first. Confirm whether your structure is modular, manufactured, or portable before you talk to a lender.

- Check your land status. Land ownership and foundation status can make or break prefab loan approvals. If you don't own land yet, factor that into your financing plan.

- Pull your credit report. Know your score before a lender does. Dispute any errors at least 60 days before applying.

- Get written cost estimates. Lenders want documentation. A written quote from your builder, including delivery and site prep, strengthens your application.

- Compare at least three lenders. Rates and terms vary widely for prefab loans. Don't accept the first offer.

Common pitfalls to avoid:

- Ignoring foundation requirements: Assuming any prefab qualifies for a standard mortgage is a costly mistake.

- Missing USDA eligibility: Many rural Kentucky and Ohio buyers skip this option without checking.

- Underestimating total project cost: Financing only the building and forgetting site work creates budget problems.

- Skipping the title check: If you're buying land and a building together, confirm the land title is clear before applying.

Pro Tip: Secure your land title and get written cost estimates in hand before you submit any loan application. Lenders move faster and offer better terms when your paperwork is complete from day one.

For a broader look at your options, the building types overview is a useful starting point. And if you want a lender's perspective on the full process, modular home buying tips from NerdWallet covers the key checkpoints clearly.

Explore flexible prefab building financing with EZ-Cabin

You now have a clear picture of how prefab financing works and which path fits your goals. The next step is finding a builder that makes the process just as straightforward as the loan itself.

At EZ-Cabin, we've built our entire process around removing the friction that slows buyers down. Our financing options include guaranteed approval rent-to-own plans with no credit check required and only the first month's payment needed to get started. No lengthy applications, no hidden fees, no waiting weeks just to find out if you qualify. You can shop prefab cabins and storage online right now, use our AI-powered customization tools to design your space, and schedule delivery in one simple workflow. Most buildings arrive within one to four weeks. If you prefer to see our buildings in person, visit our locations in London, KY or Somerset, KY.

Frequently asked questions

Do modular and manufactured homes qualify for the same loans in Kentucky and Ohio?

Modular homes on permanent foundations qualify for standard mortgages including conventional, FHA, VA, and USDA, while manufactured homes have a narrower set of qualifying loan products tied to HUD code compliance and foundation type.

Can I finance a prefab storage building or cabin with no credit check?

Yes. Rent-to-own dealer plans typically do not require a credit check, making them a practical option for storage buildings, cabins, and other non-residential prefab structures where traditional mortgage products don't apply.

How does the USDA loan for prefab homes work in rural Kentucky and Ohio?

USDA loans offer 100% financing for eligible rural buyers with a 640+ credit score, as long as the prefab home is at least 400 square feet and placed on a permanent foundation in a USDA-designated rural area.

What affects monthly payments for a prefab building loan?

Monthly payments depend on the total building cost, loan type, interest rate, and whether the structure is modular or manufactured. Prefab modular homes typically carry lower monthly payments than site-built homes because the base purchase price is lower.

Do I need to own land before getting prefab building financing?

Land ownership isn't always required, but land and foundation status significantly strengthens your loan application and can reduce your required down payment across most loan types.