TL;DR:

- Rent-to-own offers a no-credit-check option for portable buildings over 60 months.

- Total costs typically exceed cash prices due to implicit financing built into payments.

- Buyers should carefully review contracts, delivery access, and long-term affordability before signing.

Rent-to-own sounds simple on the surface: make monthly payments, get a building at the end. But the reality involves financing structures, repossession risks, and total costs that most buyers never see coming. If you're in Kentucky or Ohio and you're looking at portable buildings, cabins, or tiny homes without a traditional credit check, a 60 month rent-to-own agreement might be your best path forward. This article breaks down exactly how it works, what it costs, and what to watch out for before you sign anything.

Table of Contents

- What is a 60 month rent-to-own agreement?

- How much does a 60 month rent-to-own really cost?

- Pros and cons of 60 month rent-to-own for KY and OH buyers

- What to check before you sign a 60 month rent-to-own agreement

- The truth about rent-to-own in 2026: Hard lessons for buyers

- Next steps: Secure your portable building with flexible financing

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Simple qualification | 60 month rent-to-own lets KY/OH buyers with no credit buy portable buildings or cabins with minimal paperwork. |

| Higher total cost | Rent-to-own is more expensive than cash due to implicit financing—even without stated interest rates. |

| Repossession risk | Missing payments can lead to repossession, so making every payment on time is essential. |

| Checklist for safety | Before signing, check delivery options, read the fine print, and verify tax responsibilities. |

| Flexible uses | Rent-to-own options are ideal for portable homes, cabins, offices, and sheds on your property. |

What is a 60 month rent-to-own agreement?

A 60 month rent-to-own agreement is a contract where you make fixed monthly payments on a portable building, cabin, or shed for five years. At the end of that term, ownership transfers to you. No bank loan. No credit approval. Just a payment plan managed directly through the dealer or a leasing partner.

This structure is especially popular in Kentucky and Ohio because it opens the door for buyers who can't qualify for traditional financing. You don't need a strong credit score, and in most cases, you don't need a credit check at all. Programs like guaranteed no-credit shed financing make it possible to get approved the same day you apply.

The most common use cases include:

- Backyard storage sheds for homeowners who need extra space fast

- Portable cabins used as guest rooms, home offices, or hobby spaces

- Tiny homes for people transitioning to smaller, more affordable living

- Garages and workshops for small business owners or tradespeople

The typical process looks like this:

- Choose your building and confirm your delivery location is accessible

- Review the payment schedule and total cost

- Sign the rent-to-own contract

- Pay the first month's payment to get started

- Receive delivery within 1 to 4 weeks

- Make monthly payments for 60 months

- Take full ownership once the final payment clears

At the end of the 60 months, the building is yours. However, some edge cases include late payment repossession, forfeiture of payments already made, late fees, and taxes due at the point of ownership transfer. Some dealers also use third-party leasing partners like C3 to manage contracts, which adds another layer to the agreement you'll want to understand upfront.

Pro Tip: Before you confirm delivery, verify that your property has clear, unobstructed access. Some fenced yards or properties with narrow gates do not qualify for portable building delivery.

Buyers who want to explore portable building financing in KY and OH will find that the no-credit-check model is widely available, but the terms vary significantly between dealers.

How much does a 60 month rent-to-own really cost?

With the basics covered, it's critical to understand what you're really paying for with a 60 month rent-to-own plan.

The honest answer is that rent-to-own costs more than paying cash. That's not a flaw in the system. It's the price of accessibility. You get a building now, without credit, without a bank, and without a large upfront payment. That convenience is built into the total cost.

Here's how the numbers typically look for a mid-range portable cabin priced at $8,000 cash:

| Payment method | Upfront cost | Monthly payment | Total paid |

|---|---|---|---|

| Cash purchase | $8,000 | None | $8,000 |

| Bank loan (7% APR) | Varies | ~$158/month | ~$9,480 |

| 60 month rent-to-own | First month only | ~$200/month | ~$12,000 |

The RTO total cost exceeds the cash price because of what's called implicit financing. No explicit interest rate is stated in the contract, but the difference between what you pay over 60 months and the cash price represents the real financing cost. On a $8,000 building, that gap can reach $3,000 to $5,000 depending on the dealer.

Most buyers focus on the monthly payment and never calculate the total. That's the most common and most expensive mistake you can make.

When rent-to-own makes the most financial sense:

- You have no credit history and can't qualify for a traditional loan

- You need the building immediately and can't save for a cash purchase

- Your monthly budget is tight and the lower entry cost matters more than total cost

- You're using the building for income (home office, rental, business) and can offset the cost

The risks are real too. If you miss payments, the dealer can repossess the building and you lose everything you've paid. There's no equity protection the way there is with a mortgage. Exploring financing solutions for prefab buildings before you commit gives you a full picture of your alternatives.

Pro Tip: Ask your dealer to print out the full payment schedule showing the total amount paid over 60 months. Compare that number directly against the cash price before you sign.

Understanding the benefits of prefab sheds can also help you decide whether the long-term investment makes sense for your property and goals.

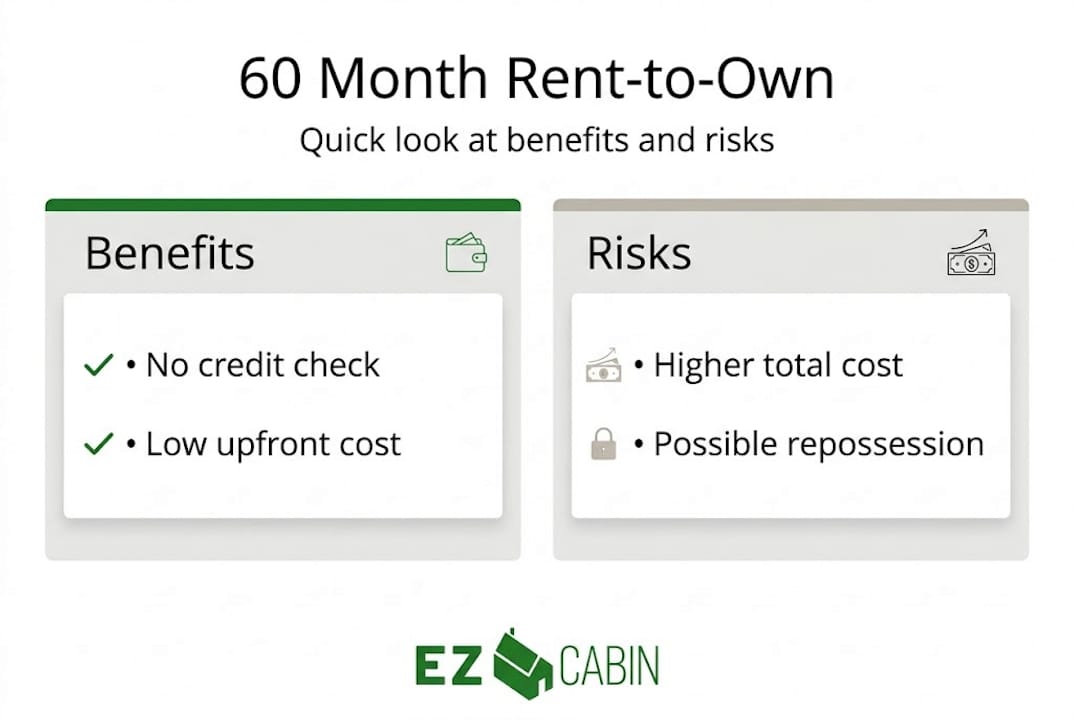

Pros and cons of 60 month rent-to-own for KY and OH buyers

Now that we know the financial details, let's weigh the benefits and drawbacks of choosing this path in Kentucky and Ohio.

| Pros | Cons |

|---|---|

| No credit check required | Total cost exceeds cash price |

| Low upfront cost (first month only) | Repossession risk if payments are missed |

| Fast delivery, usually within 4 weeks | Late fees can add up quickly |

| Flexible use: home, office, business | Forfeiture of all payments on default |

| Ownership at end of term | Taxes due at ownership transfer |

| Works on most residential properties | Some fenced or inaccessible properties excluded |

The backyard cabin benefits in Kentucky and Ohio are real. Buyers use these buildings as home offices to avoid commuting costs, as guest cabins to avoid hotel expenses for visiting family, and as hobby workshops that add genuine value to their property. For small business owners, a portable building can become a client-facing workspace or storage facility without the overhead of commercial rent.

The drawbacks deserve equal attention. Late payments risk repossession, forfeiture of payments already made, and late fees that compound quickly. Unlike a mortgage where missing one payment triggers a grace period and formal process, rent-to-own contracts can move to repossession faster than most buyers expect.

Common pitfalls to avoid:

- Signing without reading the repossession clause in full detail

- Ignoring the total cost and focusing only on monthly payments

- Assuming all properties qualify without confirming delivery access

- Forgetting about taxes owed when ownership transfers after month 60

- Skipping the comparison between rent-to-own and other available financing

For buyers who want to think long-term, modern shed investments in KY and OH show that a well-chosen portable building can increase property value and pay for itself over time, especially when used for income-generating purposes.

What to check before you sign a 60 month rent-to-own agreement

To avoid surprises and protect your investment, here's a practical checklist before you commit.

-

Confirm your delivery location qualifies. Measure gate openings, check for overhead lines, and verify the ground is accessible. Some fenced areas or properties with restricted access are not eligible for delivery.

-

Request the full cost breakdown. Ask for the total amount paid over 60 months, not just the monthly payment. Calculate the difference between that total and the cash price to understand your real financing cost.

-

Read the repossession and late fee terms. Know exactly how many days late triggers a fee, and how many missed payments lead to repossession. This information is in the contract, but it's rarely highlighted.

-

Understand the ownership transfer process. At month 60, you'll likely owe taxes on the transfer. Ask your dealer what those taxes look like in your county so there are no surprises at the finish line.

-

Ask about the leasing partner. Some dealers use third-party leasing companies like C3 to manage the contract. If that's the case, your agreement is with that company, not the dealer. Know who you're actually paying.

-

Check for early buyout options. Many rent-to-own contracts allow you to pay off the balance early at a discounted rate. This can save you thousands if your financial situation improves during the term.

"Before signing any rent-to-own contract, calculate the total you'll pay over the full term and compare it directly to the cash price. The monthly payment feels manageable, but the five-year total tells the real story." — Rent-to-own sheds: How it works, what it costs, and what to check before you sign

For buyers thinking about delivery logistics, reviewing affordable cabin delivery tips can help you prepare your property and avoid delays.

Pro Tip: Ask your dealer whether a reputable leasing partner like C3 services your area. Established leasing partners tend to have clearer contract terms and more transparent dispute processes than informal dealer agreements.

The truth about rent-to-own in 2026: Hard lessons for buyers

With all the facts in hand, here's an honest look at what really matters before you decide.

Most buyers who struggle with rent-to-own programs don't fail because the product is bad. They fail because they made a decision based on one number: the monthly payment. That single number feels manageable. It fits the budget. It gets signed. But five years is a long time, and life changes fast.

The real trap isn't the cost. It's the commitment. A 60 month rent-to-own agreement means 60 consecutive on-time payments. Miss two or three in a row during a rough patch, and you could lose the building and every dollar you've paid into it. There's no refinancing option. No grace period negotiation. No equity to fall back on.

We've seen buyers who would have been better served by a traditional loan, a personal line of credit, or even saving for a few extra months to buy outright. The RTO total cost exceeds the cash price because of implicit financing built into the payment structure. That's not hidden, but it is easy to overlook when you're focused on getting a building fast.

The buyers who get the most value from rent-to-own are the ones who treat it like a serious financial product. They run the numbers on all available options using comparisons of building financing options, confirm their budget can handle 60 months of payments without strain, and read every line of the contract before signing.

If you're genuinely unable to qualify for other financing and you need the building now, rent-to-own is a legitimate and valuable tool. Just go in with your eyes open.

Pro Tip: Only sign a 60 month rent-to-own agreement if you're confident you can make every single payment on time for five full years. Repossession isn't a theoretical risk. It happens regularly, and it's painful.

Next steps: Secure your portable building with flexible financing

You now have a clear picture of how 60 month rent-to-own works, what it costs, and what to watch for. That knowledge puts you in a much stronger position than most buyers who sign without doing the math.

At EZ-Cabin, we make the process straightforward from the start. Our flexible rent-to-own financing requires no credit check and gets you started with just the first month's payment. You can browse our full inventory, use our AI-powered tools to design your space through our custom building options, and schedule delivery all in one place. If you'd rather see a building in person before committing, visit our EZ-Cabin locations in KY and OH in London or Somerset. Most buildings deliver within 1 to 4 weeks. No hidden fees, no complicated approvals, just a building that fits your life and your budget.

Frequently asked questions

Is rent-to-own really available with no credit check for portable buildings?

Yes, most rent-to-own programs in KY and OH for cabins and sheds do not require a credit check, making them accessible to buyers with limited or no credit history.

What happens if I miss a payment in a 60 month rent-to-own agreement?

Missing payments can lead to repossession, late fees, and forfeiture of all payments already made, so consistent on-time payments are essential.

Do I pay more with rent-to-own compared to buying a building outright?

Yes, the total rent-to-own cost usually exceeds the cash price because implicit financing is built into the monthly payment structure over 60 months.

Are there any restrictions on where rent-to-own buildings can be delivered?

Yes, some fenced areas or properties with poor access may not qualify for delivery, so always confirm your site before signing.

Will I owe any extra fees or taxes at ownership transfer?

Yes, buyers are responsible for any taxes due at transfer when ownership officially moves to you after the 60th payment clears.